A new standard VAT return, which could cut costs for EU businesses by up to EUR 15 billion a year, is proposed by the European Commission. The aim of this initiative is to slash red tape for businesses, ease tax compliance and make tax administrations across the Union more efficient. As such, the Commission says it it fully reflects its commitment to ‘smart regulation’ and is one of the initiatives set out in the recent REFIT to simplify rules and reduce administrative burdens for businesses. The proposal foresees a uniform set of requirements for businesses when filing their VAT returns, regardless of the Member State in which they do it. The standard VAT return – which will replace national VAT returns – will ensure that businesses are asked for the same basic information, within the same deadlines, across the EU. Given that simpler procedures are easier to comply with and easier to enforce, today’s proposal should also help to improve VAT compliance and increase public revenues.

Advertisement

What is a VAT declaration?

A VAT return, or VAT declaration, is a document in which a taxpayer summarises its operations for a given period (month, quarter or year) to inform the tax administration of how much VAT he has to pay or how much VAT he should be reimbursed for that period.

Typically, a VAT declaration contains information on the amount of sales, the amount of purchases and the related VAT amounts. It also contains additional information to allow the tax administration to control that the declared amounts are consistent and valid.

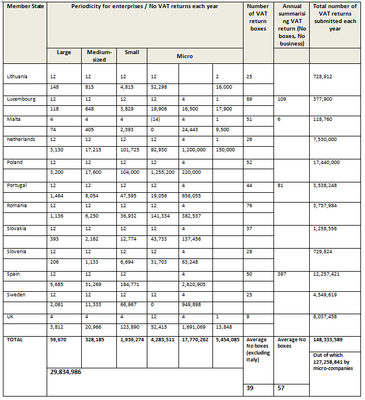

In the EU, more than 150 million VAT declarations are submitted each year, out of which almost 130 million come from micro-enterprises.

What are the main objectives of a standard VAT declaration?

The overarching objective of the standard VAT return is to make life much simpler for businesses operating in the Single Market. About 13% of all VAT taxpayers in the EU submit VAT returns in more than one Member State. Although the objectives and logic behind a VAT return are the same in all Member States, the content and format of VAT returns vary significantly from one Member State to the other. This is a source of complexity and administrative burden for businesses. In fact, VAT has been identified as one of the main sources of administrative burden by the High Level Group on Administrative Burden (Stoiber Group), with the process of declaring VAT particularly singled out by businesses. The proposed standard VAT return seeks to redress this problem, by ensuring a simple structure and standardised information and deadlines for VAT declarations across the EU.

Another benefit of the standard VAT return is that, in simplifying the process for taxpayers, it should also improve tax compliance and reduce the VAT Gap. As such, it could increase income to the public purse and contribute to growth-friendly fiscal consolidation across the EU.

This proposal was also announced in the Commission’s recent REFIT Communication.

What are the new measures proposed?

The Commission proposes to have a common format for the VAT returns applicable in all Member States. This format will contain 5 mandatory information boxes.

The mandatory information will be: chargeable VAT, deductible VAT, net VAT amount (payable or receivable), total value of input transactions and total value of output transactions.

In addition Member States will be entitled to ask for up to 21 boxes of additional information, covering, for example, the split between tax rates or details of cross-border transactions. These optional boxes are to cater for the specific needs of different tax administrations. For example, Denmark uses only one rate, so the split between tax rates would be superfluous.

The content of the 5 + 21 information boxes will be exactly the same in all Member States. In practice, it means that a taxpayer filling a VAT return in its own Member State will be able to understand and fill a VAT return in any other Member State.

The Commission also proposes to harmonise the periodicity of the returns, the submission deadlines, the procedures to submit corrections and the format of electronic submission of returns.

The proposed declaration period is one month with an optional quarterly period for micro businesses (under EUR 2 million annual turnover). Member States may allow longer periods not exceeding one year.

How have the provisions of the new standard declaration been decided?

After a broad public consultation on the EU VAT system launched with the Green Paper on the future of VAT in 2010, the Commission adopted a Communication on the future of VAT on 6 December 2011, in which it committed to put forward a proposal for a Standard VAT Declaration by the end of 2013.

The concept of a standard VAT declaration was presented in the Staff Working Paper which accompanied the Green Paper. The comments received from stakeholders were positive. In particular, respondents strongly supported the introduction of a standardised EU VAT return available in all EU languages. Both businesses and Member States were generally supportive of a Standard VAT Declaration.

In addition, the High-Level Group of Independent Stakeholders on Administrative Burdens, chaired by Mr. Edmund Stoiber, considered that administrative burdens can be reduced on VAT declarations. The Group has given opinions on the frequency and the authority to sign VAT declarations. When having tried to identify unnecessary reporting and information requirements in the context of the Commission’s Action Programme for Reducing Administrative Burdens in the European Union, VAT related burdens ranked at the top.

Businesses and Member States have been consulted during the study undertaken by PwC which included a Fiscalis seminar organised in October 2012. In addition, businesses have been further consulted in meetings of the VAT Expert Group in January 2012 and in the meeting with SME stakeholders in April 2013, and Member States in the Group on the Future of VAT held in January 2013.

Why has the Commission chosen to make the standard VAT return mandatory?

When preparing today’s proposal, the Commission carried out an Impact Assessment which calculated the overall costs and benefits of compulsory and optional Standardised VAT Declarations.

The result of the analysis was that the mandatory Standardised VAT Declaration is the best option. It avoids national tax administrations from having to deal with two different formats of VAT returns, and reduces the loopholes that can be used for tax evasion purposes.

In addition, all businesses across the EU whether operating cross border or not can benefit from the simple structure and clear deadlines set down in the proposed standard VAT return, and the specific needs of micro-enterprises have been taken fully on board in the proposal.

The optional boxes for Member States to include in the standard VAT return, depending on their own legislation and control methods ensures that the system has the necessary flexibility.

What languages can be used to fill the standard VAT return?

The form has to be submitted in the language of the country of submission. However, since the content of the information boxes will be the same in all EU countries, and the description will be available in all EU languages, it will be very easy to understand what is expected or to file a return in a foreign language.

How has the Commission calculated the EUR 15 billion a year EU businesses could save?

In the Impact Assessment, a standard cost model was applied to estimate the economic impact of the proposal. The impact was measured against meeting the main objectives of removing obstacles to cross-border trade and reducing administrative burdens on business. On that basis, it was estimated that the removal of obstacles to cross-border trade results in an overall economic benefit of 3 to 6 billion. Reducing administrative burdens adds another 9 billion in benefits. This brings the overall benefits of a standard VAT return to 15 billion a year.

What are the next steps?

The Commission’s proposal will have to be adopted by Member States in the Council, after consultation of the European Parliament. The Directive should enter into force on 1st January 2017.

Annex – Total population and total number of VAT returns