Capital requirements directive revision - guide

20 July 2011by eub2 -- last modified 20 July 2011

Banks have been at the centre of the financial crisis the global economy is facing since 2008. Lessons have been drawn from this and mistakes of the past should not repeat themselves. This is why the European Commission has brought forward today proposals to change the behaviour of the 8000 banks that operate in Europe The overarching goal of this proposal is to strengthen the resilience of the EU banking sector while ensuring that banks continue to finance economic activity and growth.

Advertisement

Why is the Commission proposing a revision of the Capital requirements directive?

The financial crisis revealed vulnerabilities in the regulation and supervision of the (European) banking system.

The package proposed today builds on the lessons learnt from the recent crisis that has shown that losses in the financial sector can be extremely large when a downturn is preceded by a period of excessive credit growth. Institutions entered the crisis with capital of insufficient quantity and quality. To safeguard financial stability, governments had to provide unprecedented support to the banking sector in many countries (1).

The overarching goal of the today's proposal is to strengthen the resilience of the EU banking sector so it would be better placed to absorb economic shocks while ensuring that banks continue to finance economic activity and growth.

What lessons have we learnt from the crisis?

First and foremost the crisis revealed an absolute necessity of enforcing the cooperation of monetary, fiscal and supervisory authorities across the globe. Cross border developments were observed too late, cross border impacts were very difficult to analyse.

Secondly, some institutions in the financial system appeared to be resilient and ready to absorb also enormous market shocks. Other institutions, even with similar capital levels, appeared to be unable to protect themselves. The crucial differences between the two were found in: the quality and the level of the capital base, the availability of the capital base, liquidity management and the effectiveness of their internal and corporate governance. These lessons justified amending the Basel agreement, and accordingly replacing the CRD with a new regulatory framework.

Thirdly, cross border failures of international financial groups appeared an insurmountable challenge for nationally accountable authorities; as a consequence, several banks needed the intervention of the state in order to stay afloat. The knowledge that banks could have been resolved, also in a cross border context, would have changed the balance of power between public authorities and banks, with the former having more tools at their disposal than just the public purse and the bail-out option, and the latter not being able to enjoy the best of all worlds: privatize gains, socialize losses. This would have put a dent on bank's risk appetite. This justifies the Commission's bank resolution framework, to be presented later this year.

Why did existing rules (including Basel 1/Basel 2) not stop the crisis from happening?

Basel 1 aimed to build a general minimum base of own funds in every bank; the rule was that 8% of the total balance sheet should be backed by own funds in order to absorb losses that could not be absorbed by its creditors.

Basel 2 was a response to the observation that the required capital base had invited banks to seek for business that had a higher expected return while the inherent higher risk profile did not lead to a higher capital requirement. So, under Basel 2 banks need to hold more capital for higher risk. The Basel 2 framework was implemented in Europe on 1 January 2008, half a year after the start of the crisis.

Basel 2.5 meant to enhance the main shortcomings of Basel 2 related to the banks' trading book and complex securitisations. Basel 2.5 was meant to be implemented from 1 January 2011, but requires implementation across the globe. However, the US was unable to implement on time, which pushed back the implementation timescale in the EU to 31 December 2011.

On top of the above shortcomings, the following factors also contributed to the crisis: capital that was actually not loss-absorbing, failing liquidity management, inadequate group wide risk management and insufficient governance. These are now included in CRD IV.

How does this proposal relate to the stress tests results released last week?

They complement each other. The results of the union-wide assessment of the resilience of EU banks to adverse market developments foreseen under the 2010 EBA regulation (1093/2010) were released last week. The test highlighted that a number of banks needed to strengthen their capital base to better withstand market turmoil in the short term.

This proposal applies to all EU banks (more than 8,300). It strengthens their resilience in the long term by increasing the quantity and quality of capital they have to hold. This makes the EU banking system better able to withstand losses should they materialise, thereby reducing the likelihood of default or need for public support.

The proposal also contains provisions on stress tests that strengthen the union-wide ones. The proposal for a directive notably states professional secrecy shall not prevent competent authorities from publishing the outcome of the union-wide stress tests and from transmitting the outcome to the EBA for purposes of publication.

It also complements the EU-wide stress tests. Indeed, the proposal for a directive states that competent authorities shall carry out annual supervisory stress tests on institutions they supervise if their supervisory reviews of individual institutions highlight the need for such tests and the union-wide ones do not sufficiently address the problems found during the supervisory review.

BASEL III, CRD IV AND INTERNATIONAL LEVEL PLAYING FIELD

What is the Basel Committee?

The Basel Committee on Banking Supervision (BCBS) has the task of developing international minimum standards on bank capital adequacy. It is based at the headquarters of the Bank for International Settlements (BIS) in Basel, Switzerland. The members come from Argentina, Australia, Belgium, Brazil, Canada, China, France, Germany, Hong Kong SAR, India, Indonesia, Italy, Japan, Korea, Luxembourg, Mexico, the Netherlands, Russia, Saudi Arabia, Singapore, South Africa, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States. The European Commission and the European Central Bank are observers.

What is "Basel III"?

The BCBS develops minimum standards on bank capital adequacy. These have evolved over time. Following the financial crisis, the Basel Committee has reviewed its capital adequacy standards. Basel III is the outcome of that review, with the number three coming from it being the third configuration of these standards. (2)

What is "Basel III" proposing to make banks stronger?

Better and more capital

Several banks appeared to have a capital base on their balance sheet meeting the regulatory standards, which, however, turned out to be not always available when needed for loss absorption. Some contracts restricted the absorption of losses or there were simply no liquid assets mirroring the balance sheet capital figure.

Basel III now prescribes 14 very strict criteria (3) that must be met by own funds instruments, in order to ensure that these own funds of the bank can effectively be used in times of stress.

More balanced liquidity

A major problem was the lack of liquid assets and liquid funding during the crisis – referred to as "the market dried up". Basel III requires bankers to manage their cash flows and liquidity much more intense than before, to predict the liquidity flows resulting from creditors' claims better than before, and to be ready for stressed market conditions by having sufficient "cash" available, both in the short term and in the longer run.

Leverage back stop

Just in case the calculated risk weights of Basel 2 and 2.5 contain errors, models contain errors, or new products are developed and risk weights are not measured precisely yet, a traditional back stop mechanism limits the growth of the total balance sheet as compared to available own funds. A maximum leverage of 12 used to be a rule of thumb in the days that banks were not regulated yet. Today, given the sophistication of risk weight determination, the leverage ratio will be an additional checking tool for supervisors.

As this tool is new for the international framework, it was agreed that data and experience must be gathered before an effective leverage ratio can be introduced as a binding requirement in each jurisdiction.

Capital requirements for derivatives (Counter party credit risk)

Basel 3 also introduces risk weights for what is called counterparty credit risk. This is not related to an exposure booked on the balance sheet, but are related to the underlying value of a derivative instrument and the creditworthiness of the counterparty selling the derivative contract.

A derivative is an instrument whose value depends on another instrument, another "underlying value". Derivatives are used for good reasons in banks' risk management, but the crisis revealed that exposures and losses could be material, and that a specific treatment in the supervisory framework was justified.

The framework invites banks to use central counterparties (CCPs) for their derivatives, which must prevent situations in which one important market participant's failure affects other dealers. CCP is an entity that interposes itself between the two counterparties to a transaction, becoming the buyer to every seller and the seller to every buyer. A CCP's main purpose is to manage the risk that could arise if one counterparty is not able to make the required payments when they are due –i.e. defaults on the deal.

Conservation buffer

The conservation buffer is a fixed target buffer of 2.5% meant for a specific objective, preventing the situation in which taxpayers' money would have to be injected for recovery and resolution of banks.

The crisis triggered capital injections, backed by taxpayers, to save institutions that didn't have sufficient buffers themselves to cover exceptional costs like these. All in all, the total required capital level is increased substantially (risk weighted capital base plus conservation buffer plus countercyclical buffer) while it has to be covered by instruments of much higher quality than before.

Countercyclical buffer

This refers to the buffer that is built up in good times, and used in economic downturns and represents another new element in Basel III. Requiring a higher buffer in good times also prevents that credit becomes so cheap, because risk profiles seem safe, that exposures are built up in an excessive way. This extra buffer can be used when the economic development goes down, in order to prevent that credit becomes so expensive, because risk profiles show more and more expected losses, that banks reduce their exposures in an excessive way. The countercyclical buffer is meant to stabilize the supply of credit in an economy. Since dynamics can be very different across different markets, these buffers are determined on a national market base.

Does the CRD IV proposal fully implement "Basel III"?

The Commission has actively contributed to developing the new capital, liquidity and leverage standards in the Basel Committee on Banking Supervision, while making sure that major European banking specificities and issues are appropriately addressed.

The Commission's proposal therefore respects the balance and level of ambition of Basel III. However, there are two reasons why the Commission cannot simply copy/paste Basel III into its legislative proposal.

First, Basel III is not a law. It is the latest configuration of an evolving set of internationally agreed standards developed by supervisors and central banks. That has to now go through a process of democratic control as it is transposed into EU (and national) law. It needs to fit with existing EU (and national) laws or arrangements. As EU law takes precedence over national law, the Commission's proposal launches that process.

Furthermore, while the Basel capital adequacy agreements apply to 'internationally active banks', in the EU it has always applied to all banks (more than 8,300) as well as investment firms.4 This wide scope is necessary in the EU where banks authorised in one Member State can provide their services across the EU's single market and as such are more than likely to engage in cross-border business. Also, applying the internationally agreed rules only to a subset of European banks would create competitive distortions and potential for regulatory arbitrage.

The Commission has had to take these particular circumstances into account when transposing Basel III into EU law. Nevertheless, the proposal delivers a faithful implementation of Basel III in EU law. This is important, as consistent implementation of Basel III across the globe is necessary in order to improve the resilience of the global financial system and ensure a level playing field.

What is Europe adding to "Basel III"?

As explained above, the most fundamental change is that, in implementing the Basel III agreement within the EU, we move from a uni-dimensional type of world where you have only capital as a prudential reference, to multi-dimensional regulation and supervision, where you have capital, liquidity and the leverage ratio – which is important, because this covers the whole balance sheet of the banks. And even within capital, there is a much cleaner definition and more realistic targets.

In addition to Basel III implementation, the proposal introduces a number of important changes to the banking regulatory framework.

In the Directive:

enhanced governance: the proposal strengthens the requirements with regard to corporate governance arrangements and processes and introduces new rules aimed at increasing the effectiveness of risk oversight by Boards, improving the status of the risk management function and ensuring effective monitoring by supervisors of risk governance.

sanctions: The proposal will ensure that all supervisors can apply sanctions if EU rules are breached, for example administrative fines of up to 10% of an institution's annual turnover, or temporary bans on members of the institution's management body. These sanctions should be deterrent but also effective and proportionate.

enhanced supervision: the Commission proposes to reinforce the supervisory regime to require the annual preparation of a supervisory programme for each supervised institution on the basis of a risk assessment, greater and more systematic use of on-site supervisory examinations, more robust standards and more intrusive and forward-looking supervisory assessments

Finally, the proposal will seek to reduce to the extent possible reliance by credit institutions on external credit ratings by: a) requiring that all banks' investment decisions are based not only on ratings but also on their own internal credit opinion, and b) that banks with a material number of exposures in a given portfolio develop internal ratings for that portfolio instead of relying on external ratings for the calculation of their capital requirements.

In the Regulation:

-a "single rule book": The proposal creates for the first time a single set of harmonised prudential rules which banks throughout the EU must respect. EU heads of state and government had called for a "single rule book" in the wake of the crisis. This will ensure uniform application of Basel III in all Member States, it will close regulatory loopholes and will thus contribute to a more effective functioning of the Internal Market. The Commission suggests removing national options and discretions from the CRD, and achieving full harmonisation by allowing Member States to apply stricter requirements only where these are a) justified by national circumstances (e.g. real estate), b) needed on financial stability grounds or c.) because of a bank's specific risk profile.

How do you ensure an international level playing field?

The financial system is global in nature and it is not stronger than its weakest link. It is therefore important that all countries implement international banking standards, including Basel III.

Following the adoption of the Dodd Frank Act in July 2010, the US is preparing to implement the Basel international standards. The Commission has continuous and constructive discussions with US authorities – notably via the EU-US Financial Markets Regulatory Dialogues – regarding their implementation of the Basel II and Basel III agreements in a proper and timely manner.

What are the timelines and implementation in other G20 countries?

The Commission proposal follows the timelines as agreed in the Basel Committee: entry into force of the new legislation on 1 January 2013, and full implementation on 1 January 2019. The EU is the first jurisdiction publishing its Basel III based legislative proposal, but all G20 members committed to doing so in due course and implement as agreed. The Commission intends to monitor closely relevant international developments in this respect.

In this context, it's worth recalling that unlike some other major economies, the EU is not limiting the application of the Basel III reforms to only internationally active banks, but will apply them across its banking sector to cover all banks and in general also investment firms.

What will you do if other jurisdictions do not implement?

The EU has an interest in increasing the resilience of its banking system. As Basel III aims to achieve that objective, it is in principle in our interest to implement it. While there is always a short term risk of regulatory arbitrage if one jurisdiction goes further than other jurisdictions, in the longer term it is clearly beneficial as market participants benefit from a stable, safe and sound financial system. Even so, there may be areas where an international level playing field is more important also in the short run (e.g. the new elements of Basel III). The Commission is therefore closely monitoring the consistent implementation of Basel III across the globe and would need to draw all the necessary conclusions in due time should other key jurisdictions not follow suit.

STRUCTURE OF PROPOSAL

Why does the proposal contain two legal instruments? Why also a regulation?

The proposal divides the current CRD (Capital Requirements Directive) into two legislative instruments: a directive governing the access to deposit-taking activities and a regulation establishing the prudential requirements institutions need to respect.

While Member States will have to transpose the directive into national law, the regulation is directly applicable, which means that it creates law that takes immediate effect in all Member States in the same way as a national instrument, without any further action on the part of the national authorities. This removes the major sources of national divergences (different interpretations, gold-plating). It also makes the regulatory process faster and makes it easier to react to changed market conditions. It increases transparency, as one rule as written in the regulation will apply across the single market. A regulation is subject to the same political decision making process as a directive at European level, ensuring full democratic control.

Last but not least, this proposal marks a thorough review of EU banking legislation that has developed over decades. The result is a more accessible and readable piece of legislation.

What goes in which instrument?

Areas of the current CRD where the degree of prescription is lower and where the links with national administrative laws are particularly important will stay in the form of a directive. This concerns in particular the powers and responsibilities of national authorities (e.g. authorisation, supervision, capital buffers and sanctions), the requirements on internal risk management that are intertwined with national company law as well as the corporate governance provisions. By contrast, the detailed and highly prescriptive provisions on calculating capital requirements take the form of a regulation.

|

Directive (Strong links with national law, less prescriptive) |

Regulation (Detailed and highly prescriptive provisions establishing a single rule book) |

|

Access to taking up/pursuit of business |

Capital |

|

Exercise of freedom of establishment and free movement of services |

Liquidity |

|

Prudential supervision |

Leverage |

|

Capital buffers |

Counterparty credit risk |

|

Corporate governance |

|

|

Sanctions |

SINGLE RULE BOOK

What is the single rule book?

In June 2009, the European Council called for the establishment of a "European single rule book applicable to all financial institutions in the Single Market." The single rule book aims to provide a single set of harmonised prudential rules which institutions throughout the EU must respect. This will ensure uniform application of Basel III in all Member States. It will close regulatory loopholes and will thus contribute to a more effective functioning of the Single Market. The Commission suggests removing national options and discretions from the CRD, and achieving full harmonisation by allowing Member States to apply stricter requirements only where these are needed on financial stability grounds or because of a bank's specific risk profile.

Why is the single rule book important?

Today, European banking legislation is based on a Directive which leaves room for significant divergences in national rules. This has created a regulatory patchwork, leading to legal uncertainty, enabling institutions to exploit regulatory loopholes, distorting competition, and making it burdensome for firms to operate across the Single Market.

For example:

Securitisation was at the core of the financial crisis. Previous global and EU standards (Basel II, CRD I) addressed some of the risks by specific capital requirements (including for all liquidity facilities). However, many Member States did not follow, benefiting from a transitional opt-out. In a fully integrated market such as securitisation, it was easy for cross-border groups to issue their securitisation titles in those Member States that opted out rather than in Member States which applied the standards.

Following the experience with securitisation in the financial crisis, CRD II introduced harmonised rules to tighten the conditions under which institutions could benefit from lower capital requirements following a securitisation (including a harmonised notion of significant risk transfer). But several Member States have not transposed this by the end of 2010 as required.

The financial crisis has shown that reliable internal risk models are important for institutions to anticipate stress and hold appropriate capital. However, requirements for, and accordingly the implementation of, internal ratings based risk models vary from one Member State to another. As a result, capital requirements for comparable exposures differ, leading potentially to an unlevel playing field and regulatory arbitrage.

A tough definition of capital is a key element of Basel III. However, experience with CRD I has shown that Member States introduced enormous variations when transposing the directive definition into national law. Even where the requirements of the directive were clear, some Member States did not correctly transpose them. In some cases, the Commission had to open infringement proceedings, taking many years, in order to force these Member States to comply with the directive. (5)

A single rule book based on a regulation will address these shortcomings and will thereby lead to a more resilient, more transparent, and more efficient European banking sector:

A more resilient European banking sector: A single rulebook will ensure that prudential safeguards are wherever possible applied across the EU and not limited to individual Member States. The crisis highlighted the extent to which Member States' economies are interconnected. The EU is a shared economic space. What affects one country could affect all. It is not realistic to believe that unilateral action brings safety in this context. If a Member State increases the capital requirements for domestic institutions, institutions from other Member States can continue to provide their services with lower requirements – and at a competitive advantage - unless other countries follow suit. This gives also rise to regulatory arbitrage. Institutions affected by the higher capital requirements could relocate to another Member State and continue to provide their services in the original Member State by means of a branch.

A more transparent European banking sector: A single rulebook will ensure that institutions' financial situation is more transparent and comparable across the EU - for supervisors, deposit-holders and investors. The financial crisis has demonstrated that the opaqueness of regulatory requirements in different Member States was a major cause of financial instability. Lack of transparency is an obstacle to effective supervision but also to market and investor confidence.

A more efficient European banking sector: A single rulebook will ensure that institutions do not have to comply with 27 differing sets of rules.

Why is the Commission eliminating the possibility for Member States to require institutions to hold more capital?

The EU in general and the euro area in particular have a very high degree of financial and monetary integration. Decisions on the level of capital requirements therefore need to be taken for the single market as a whole, as the impact of such requirements is felt by all Member States. Financial stability can only be achieved by the EU acting together; not by each Member State on its own.

For example, if EU capital requirements are set too low, an individual Member State cannot escape risks to financial stability by simply increasing requirements for its own institutions. Unless other Member States follow suit, foreign institutions' branches can continue to import risk.

Higher levels of capital requirements in one Member State would also distort competition and encourage regulatory arbitrage. For example, institutions could be encouraged to concentrate risky activities in Member States which only implement the minimum requirements.

Therefore, we need to set the level of capital at a level that is appropriate for the EU as a whole. That is why the minimum capital requirements written in CRDIV cannot be increased by national authorities (e.g. 6% CET 1 instead of 4,5%), unless a specific add-on is justified following an individual supervisory review (Pillar 2, see below).

Will Member States still retain some flexibility under the Single Rule Book?

Member States will retain some possibilities to require their institutions to hold more capital. For example, Member States will retain the possibility to set higher capital requirements for real estate lending, thereby being able to address real estate bubbles. If they do, this will also apply to institutions from other Member States that do business in that Member State. Moreover, each Member State is responsible for adjusting the level of its countercyclical buffer to its economic situation and to protect economy/banking sector from any other structural variables and from the exposure of the banking sector to any other risk factors related to risks to financial stability. Furthermore, Member States would naturally retain current powers under "pillar 2", i.e. the ability to impose additional requirements on a specific bank following the supervisory review process (see below).

|

Type of Measure |

Compatible with Single Rule Book? |

||||||||||||||

|

EU Macro-prudential Measures |

|||||||||||||||

|

|

|

||||||||||||||

|

|

"Pillar 2" measures |

National supervisors can impose a wide range of measures - including additional capital requirements – on individual institutions or groups of institutions in order to address higher-than-normal risk |

Measures are included in the Directive. They have to be justified in terms of particular risks of a given institution or group of institutions, including risks pertaining to a particular region or sector. Further convergence of such measures will be sought over time. |

||||||||||||

What is "Pillar 2"? What do you propose to change?

Pillar 2 refers to the possibility for national supervisors to impose a wide range of measures - including additional capital requirements – on individual institutions or groups of institutions in order to address higher-than-normal risk. They do so on the basis of a supervisory review and evaluation process, during which they assess how institutions are complying with EU banking law, the risks they face and the risks they pose to the financial system. Following this review, supervisors decide whether e.g. the institution's risk management arrangements and level of own funds ensure a sound management and coverage of the risks they face and pose. If the supervisor finds that the institution faces higher risk, it can then require the institution to hold more capital. In taking this decision, supervisors should notably take into account the potential impact of their decisions on the stability of the financial system in all other Member States concerned. The proposal clarifies that supervisors can extend their conclusions to types of institutions that, belonging to the same region or sector, face and/or pose similar risks.

How will this affect those Member States that have already decided to go further than Basel III or are planning to do so?

Some Member States (e.g. Spain) have already decided to go above the minimum levels of capital foreseen by Basel III. Some (e.g. Sweden, Cyprus) have indicated their intention to start doing so. Others (e.g. UK) have national processes under way that consider requiring minimum level of own funds above Basel III from parts of their banking sector, even though the full details of such plans are not yet finalised. In some instances, Member States have also decided to introduce more quickly the changes foreseen under Basel III that increase the quality of capital as well.

The Commission fully shares the objective of improving the resilience of the EU banking system and considers that to do so in a sustainable way requires a single rule book, level of own funds included, applicable across the EU. Member States are free to anticipate the full implementation of Basel III and hence move to the capital requirements foreseen for 1 January 2019 already today, should they so wish. While Member States will not be able to exceed the level of own funds requirement set by the proposal, they can use the instruments of flexibility foreseen by the proposal for a regulation and directive, namely the counter-cyclical buffer to dampen excess lending growth and/or require a institution or group of institutions to hold additional capital to cover against particular risks (including financial stability) following a supervisory assessment ("Pillar 2").

CAPITAL

What is bank capital?

Capital can be defined in different ways. The accounting definition of capital is not the same as the definition used for regulatory capital purposes.

For banking prudential requirements purposes, capital is not obtained simply by deducting the value of an institution's liabilities (what it owes) from its assets (what it owns). Regulatory capital is more conservative than accounting capital. Only capital that is at all times freely available to absorb losses qualifies as regulatory capital. Additional conservatism is added by adjusting this measure of capital further by e.g. deducting assets that may not have a stable value in stressed market circumstances (e.g. goodwill) and not recognising gains that have not yet been realised.

What is the capital adequacy requirement?

It is the amount of capital an institution is required to hold compared to the amount of assets, to cover unexpected losses. In the CRD, this is called 'minimum own funds requirement' and is expressed as a percentage.

Why is capital important?

The purpose of capital is to absorb the losses that a bank does not expect to make in the normal course of business (unexpected losses). The more capital a bank holds, the more losses it can suffer before it defaults. If a firm owes more than it owns (its assets are worth less than its liabilities), it cannot pay its debt and is thereby insolvent. If a bank has less capital than the requirement amount, supervisors can take measures to prevent insolvency.

How is it calculated?

It is the value of a bank's capital as a percentage of its risk weighted assets (RWA). The formula is simple: capital / RWA > 8%.

What are risk-weighted assets?

When assessing how much capital an institution needs to hold, regulators weigh an institution's assets according to their risk. Safe assets (e.g. cash) are disregarded; other assets (e.g. loans to other institutions) are considered more risky and get a higher weight. The more risky assets an institution holds, the more capital it has to have. In addition to risk weighing on balance sheet assets, institutions have to hold capital also against risks related to off balance sheet exposures such as loan- and credit card commitments. These are also risk weighed.

What is the difference between Tier 1 and Tier 2 capital?

Capital comes in different forms that serve different purposes. There are two types of capital:

Going concern capital: this allows an institution to continue its activities and helps to prevent insolvency. The purest form is common equity (labelled CET1). Going concern capital is considered Tier 1 capital.

Gone concern capital: this helps ensuring that depositors and senior creditors can be repaid if the institution fails. One example of this kind of capital is institution debt. Gone concern capital is considered Tier 2 capital.

What was the problem with capital during the crisis?

Banks and investment firms did not all hold sufficient amounts of capital and the capital they held was sometimes of poor quality as it was not readily available to absorb losses as they materialised. To prevent institutions from defaulting, public funds had to be used to prop up institutions.

How do you propose to increase the quality and quantity of capital?

In line with Basel III, the proposal strengthens institutions' capital base by increasing the amount of own funds institutions need to hold and by restricting what counts as own funds.

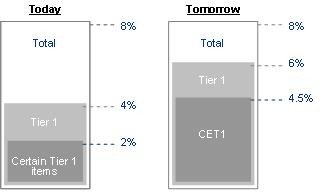

Today, banks and investment firms need to hold a minimum total capital of 8% of risk weighted assets. Tomorrow, while the total capital an institution will need to hold remains at 8%, the share that has to be of the highest quality – common equity tier 1 (CET1) – increases from 2% to 4.5%.

The criteria for each instrument will also become more stringent. Furthermore, the proposal harmonises the adjustments made to capital in order to determine the amount of regulatory capital that it is prudent to recognise for regulatory purposes. This new harmonised definition would significantly increase the effective level of regulatory capital required to be held by institutions. One unit of Basel II capital is therefore not the same as one unit of Basel III capital.

Are you only proposing to increase the former minimum level of capital?

No. In line with Basel III, the proposal also creates two new capital buffers: the capital conservation buffer and the counter-cyclical buffer (see section on capital buffers). To this new framework may in the future be added capital surcharges for systemically important banks (see section on capital buffers). Naturally, on top of these own funds requirements, supervisors may add extra capital to cover for other risks following a supervisory review (see pillar 2 below).

How can institutions increase their capital ratio to meet the new requirements?

Institutions can increase their capital ratio in two ways:

Increase capital: An institution can increase its capital by either issuing new shares and/or not pay dividends to its shareholders, i.e. to retain profits. These new shares and retained profits become included in its capital base. Provided they do not increase their RWA, this increases their capital ratio.

Reduce assets and their risk weight: An institution can also cut back on lending, sell loan portfolios and/or make less risky loans and investments, thereby reducing its risk-weighted assets, which has the effect of - for a given amount of capital - increasing its capital ratio (capital/RWA).

When will these provisions start to apply?

Basel III foresees a substantial transition period before the new capital requirements apply in full. This is to ensure that increasing the resilience of institutions does not unduly affect lending to the real economy (i.e. to ensure that institutions do not cut back on lending and investments). The provisions related to the minimum level of own funds will accordingly be phased in as of 2013. The new prudential adjustments will also be introduced gradually, 20% per annum from 2014, reaching 100% in 2018. The provision to grandfather over 10 years will also apply to certain capital instruments in order to help to ensure a smooth transition to the new rules.

Why do you allow Member States to implement Basel III faster than foreseen?

Basel III foresees a gradual transition to the stricter standards, with full implementation as of 1 January 2019. The Commission proposal foresees the same transition period but allows Member States to implement the stricter definition and/or level of capital more quickly than is required by Basel III. The reason is that some Member States have already anticipated the reforms contained in Basel III and it would be inappropriate to artificially force them to temporarily undo these desirable reforms.

Does the proposal depart from the Basel III definition of capital?

Under Basel III, CET1 capital instruments for companies that can issue ordinary shares – so-called 'joint stock companies' - may comprise only "ordinary shares" that meet 14 strict criteria. The proposal does not restrict the highest quality form of capital only to "ordinary shares". However, it takes the same approach as Basel III by imposing 14 strict criteria that any instrument would have to meet to qualify, with appropriate adaptation to the criteria for instruments issued by non-joint stock companies such as mutuals, cooperative banks and savings institutions.

This approach focuses more on the substance of a capital instrument than on its legal form. With 27 different company laws in the EU, a reference to a concept of "ordinary shares" would not ensure homogeneity of the instruments recognized in a way that clear minimum criteria for recognition of instruments would. Such a focus on substance builds on the first amendment to the Capital Requirements Directive (CRD II), adopted two years ago. This amendment recognised the fact that some EU institutions issue instruments other than ordinary shares, the loss absorbency of which can be equivalent to that of ordinary shares.

By requiring that an instrument has to meet the Basel III criteria, the proposal ensures that only the highest quality instruments qualify as bank capital.

What are the conditions capital instruments have to meet to qualify as Common Equity Tier 1 instruments?

Article 26 of the proposal for a regulation states that capital instrument can only qualify as Common Equity Tier 1 instruments if a number of conditions are met. These can be summarised as follows (for full details, see article):

they are issued directly by the institution;

they are paid up and their purchase is not funded by the institution;

they meet a number of conditions as regards their classification (e.g. they qualify as capital for accounting and insolvency purposes);

they are clearly and separately disclosed on institutions' financial statements balance sheet;

they are perpetual;

the principal amount of the instruments may not be reduced or repaid unless the institution is e.g. liquidated. Moreover, the provisions governing the instruments should not indicate that the principal amount of the instruments would or might be reduced or repaid other than in the liquidation of the institution;

the instruments meet a number of conditions as regards distributions (e.g. no preferential distributions,, distributions may be paid only out of distributable items, the conditions governing the instruments do not include a cap or other restriction on the maximum level of distributions, the level of distributions is not determined on the basis of the amount for which the instruments were purchased, etc…);

compared to all the capital instruments issued by the institution, the instruments absorb the first and proportionately greatest share of losses as they occur, and each instrument absorbs losses to the same degree as all other Common Equity Tier 1 instruments;

the instruments rank below all other claims in the event of insolvency or liquidation of the institution;

the instruments entitle their owners to a claim on the residual assets of the institution, which, in the event of its liquidation and after the payment of all senior claims, is proportionate to the amount of such instruments issued and is not fixed or subject to a cap;

the instruments are not secured, or guaranteed by any entity in the group (e.g. the institution, its subsidiaries, the parent institution or its subsidiaries, etc);

the instruments are not subject to any arrangement that enhances the seniority of claims under the instruments in insolvency or liquidation.

These conditions ensure that only the highest quality capital instruments qualify as CET1.

Why is your proposal potentially recognising any instrument as Common Equity Tier 1, including silent partnerships, and not ordinary shares only?

'Silent partnership' is a generic term covering contracts where a silent partner is implicated in the operations of another firm by means of a capital contribution allowing the silent partner to share in the profit and loss. It is a generic term covering instruments with widely varying characteristics in terms of e.g. ability to absorb losses. Whether or not silent partnerships would qualify as CET1 depend on these characteristics.

To warrant recognition in the highest quality category of regulatory capital, a capital instrument – silent partnerships included – must be of extremely high quality and must absorb losses fully as they arise.

The 14 criteria for Common Equity Tier 1 capital agreed in Basel III are extremely strict by design. Only instruments of the highest quality would be capable of meeting them.

Provided an instrument met those strict criteria - including in respect of its loss absorbency – the Commission believes it should qualify as Common Equity Tier 1 capital.

Why do you propose that minority interests can be recognised to the extent they are used to meet also the counter-cyclical buffer, and not only the minimum capital requirements and the Capital Conservation Buffer?

Minority interests are capital in a subsidiary that is owned by other shareholders from outside the group. They are particularly important in the EU, as EU banking groups often have subsidiaries that are not fully owned by the parent company but have several other owners.

Basel III recognises minority interests and certain capital instruments issued by subsidiaries (e.g. hybrids and subordinated debt) to be included in the capital of the group only where those subsidiaries are banks (or are subject to the same prudential requirements) and up to the level of the new minimum capital requirements and the capital conservation buffer.

The proposal recognises minority interests also up to the level of the new countercyclical buffer, as it would in practice be used to absorb losses within a group. Furthermore, it also recognises the importance of the countercyclical buffer as an EU macro-prudential tool and removes a potential disincentive for regulators to use it.

Why are your proposals on the recognition of hedging (when calculating amounts to be deducted for investments in unconsolidated financial entities) restrictive?

Basel III allows banks to use hedging to reduce the amount of deductions they have to make from capital for investments in instruments issued by other financial institutions. The rationale is that hedging reduces the losses a bank could make from changes in the value of investments that are hedged.

That approach could transfer the risk of holdings for long-term investment or trading purposes in financial institutions outside of the banking sector. Firms not subject to a similar requirement for deduction would be likely to provide hedges to banks for their investments and would not therefore be required to make a similar deduction.

The proposal addresses this risk by limiting recognition of such hedging to the trading book only. The Commission believes there are strong reasons to do so:

First, it is difficult to hedge an instrument that is perpetual and held to maturity in the banking book.

Second, it limits the extent to which such risk can be shifted to another sector not subject to the same treatment.

Third it reduces the difficulty of establishing who ultimately bears the risk on investments in financial institutions.

Why do you propose to allow significant holdings in other financial entities like insurance companies to be exempt from deduction?

Institutions must hold a certain amount of high quality funds to absorb any significant losses they make in the course of business. Accountants define capital as the difference between assets and liabilities. However, the accounting definition does not deal with important risks to which an institution is subject and has to be adjusted accordingly by bank regulation. Such adjustments include deductions, which reduce the amount of capital that is recognised.

Basel III requires banks to deduct significant investments in unconsolidated financial entities, including insurance entities, from the highest quality form of capital (CET1). The objective is to prevent the double counting of capital, i.e. to ensure that the bank is not bolstering its own capital with capital that is also used to support the risks of an insurance subsidiary.

In the EU, groups that contain significant banking / investment businesses and significant insurance businesses are a common and important feature of the banking system. This so-called 'bancassurance' business model is a key feature of the EU banking landscape. The EU has a specific legal mechanism, the Financial Conglomerates Directive (FICOD), to address the risk of double counting of capital across the banking and insurance sectors. The FICOD is based on the international standards set out by the Joint Forum and allows consolidation of banking and insurance entities in a group. (6)

In this context, the proposal allows a more robust and consistent version of the FICOD approach to continue to be used as an alternative to a Basel III deduction approach. The fundamental review of the FICOD planned for 2012 should allow any further changes required to be made to this EU approach.

Why will you not require certain Deferred Tax Assets (DTAs) to be deducted?

Deferred Tax Assets (DTAs) are assets that may be used to reduce the amount of future tax obligations. Basel III treats DTAs differently depending on how much they can be relied upon when needed to help a bank to absorb losses. Where their value is less certain to be realised, they must be deducted from capital.

The proposal clarifies that DTAs that are transformed on a mandatory and automatic basis into a claim on the state when the firm makes a loss would be one of the forms of DTAs for which deduction would not be warranted.

This legal instrument was not discussed explicitly at the time of the Basel III agreements since it has only been introduced thereafter. This issue is likely to become subject of further work by the BCBS.

Why do you propose to prolong the Basel I floor?

Basel II requires more capital to be held by banks for riskier business than would be required under Basel I. For less risky business, Basel II requires less capital to be held than Basel I. This is what Basel II was designed to do: to be more risk sensitive.

To ensure banks do not hold too little regulatory capital, Basel II set a floor on the amount of capital required, which is 80% of the capital that would be required under Basel I.

While the floor required by the original CRD expired by the end of 2009, the CRD III reinstated it until end-2011.

In the light of the continuing effects of the financial crisis in the banking sector and the extension of the Basel I floor adopted by the Basel Committee on Banking Supervision in July 2009, the proposal reinstates the floor in 2013, to be applied until 2015. However, national authorities would be able to waive the requirement under strict conditions.

It also introduces a requirement for a continuous revision of the need for such a floor since it should not be maintained in place longer than is strictly necessary.

Why do you propose to continue recognising instruments issued after the date of agreement of the new rules in Basel?

To ensure a smooth transition to the new Basel III rules, instruments that are currently used that do not meet the new rules have to be phased out over a 10-year period, provided they were issued prior to the date of agreement of the new rules by Basel (12 September 2010). Under Basel III, instruments issued after the 'cut off date' would need to comply with the new rules or would not be recognised from 1 January 2013.

The proposal sets the cut off date as the date of adoption of the proposal by the Commission, i.e. the day when the Commission as a College agreed to legally implement Basel III in the EU. Setting a cut off date prior to this policy decision would neither be legitimate nor legally sound, as it would apply the new rules retroactively.

Why do you propose a long phasing out of instruments no longer eligible as CET1?

In 1998, Basel stated that ordinary shares are the key element of capital for companies that may issue shares, so-called joint stock companies. Given this starting point, Basel III simply derecognizes the instruments issued by joint stock companies that are not ordinary shares from 1 January 2013.

CRD II (adopted in 2009) took a different approach, focusing on the quality of capital rather than what instruments are called. Provided they are in substance as robust as ordinary shares, CRD II recognizes in the highest quality form of capital instruments issued by joint stock companies that do not take the legal form of an ordinary share.

In light of these different starting points, in the EU, rather than simply derecognizing instruments issued by joint stock companies that are not ordinary shares, the proposal phases them out over a 10-year period. In line with Basel III, the proposal recognises in capital for a 5-year period any instrument injected by a government prior to a certain date.

The proposal requires institutions to hold more capital against investments in hedge funds, real estate, venture capital and private equity than they have done to up now. Why is that?

The current CRD (points 66-67 of Annex VI, Part 1) states that competent authorities may apply a 150% risk weight to "exposures associated with particularly high risks such as investments in venture capital firms and private equity investments". However, what 'particularly high risks' are has not been defined. The lack of obligation combined with the lack of a clear definition has led to different assessments and risk weights granted to the same type of exposures. On the basis of an advice from CEBS (Committee of European Banking Supervisors, the predecessor of EBA), the Commission now proposes to require banks to assign a 150% risk weight to these types of exposures (investments in venture capital firms, alternative investment funds and speculative real estate financing as well as "exposures that are associated with particularly high risks"). The proposal now also clearly defines the criteria that supervisors should use when an exposure is associated with such risks and requires EBA to develop guidelines in that respect.

What is the role of contingent capital in the proposal?

The proposal for a regulation requires all instruments recognised in the Additional Tier 1 capital of a credit institution or investment firm to be written down, or converted into Common Equity Tier 1 instruments, when the Common Equity Tier 1 capital ratio of the institution falls below 5.125%. The proposal does not recognise other forms of contingent capital for the purposes of meeting regulatory capital requirements.

What is hybrid capital? What role does it play?

Hybrid capital is a term used to describe forms of capital instrument that have features of both debt and equity instruments. Such instruments in issue during the crisis proved not to be sufficiently loss absorbent. The proposal builds upon the improvements made under CRD II to the quality of hybrid Tier 1 capital instruments, introducing stricter criteria for their inclusion in Additional Tier 1 capital. As explained above, this includes a requirement for all such instruments to absorb losses by being written down, or converted into Common Equity Tier 1 instruments, when the key measure of a credit institution or investment firm's solvency - the Common Equity Tier 1 capital ratio - falls below 5.125%.

Is the capital definition under CRD IV in line with the definition used in the recently published stress tests?

The criteria for the highest quality regulatory capital instruments - Core Tier 1 capital - used in the recent EBA stress tests are very similar to those of this proposal. However, the proposal also introduces further significant improvements, such as new, harmonised regulatory adjustments to Common Equity Tier 1, stricter definitions of Additional Tier 1 and Tier 2 capital and phasing in of the new rules.

LIQUIDITY

What does the Commission propose on liquidity buffers?

The crisis has shown that institutions' did not hold sufficient liquid means (e.g. cash). When the crisis hit, many firms were short of liquidity. This contributed to the demise of several financial institutions. While a number of Member States currently impose some form of quantitative regulatory standard for liquidity, no harmonised regulatory treatment exists at EU level.

Basel III introduces two new ratios and foresees in each case an observation period in order to identify and address possible unintended consequences. The BCBS would do so by making the necessary changes, if any, before 2015 or 2018, respectively.

To improve short-term resilience of the liquidity risk profile of financial institutions, the Commission proposes the introduction of a Liquidity Coverage Requirement (LCR) - after an observation and review period - in 2015. More specifically:

Institutions will be required to have appropriate liquidity coverage as of 2013.

To ensure that the observation period is meaningful, institutions will report to national authorities the elements that are needed to verify that they have adequate liquidity coverage. They should do so in a uniform way, with reporting formats to be developed by EBA.

The Commission will have a power to specify the liquidity coverage requirement based on the outcome of the observation period and international developments

As regards the net stable funding requirement, the Commission will use the longer Basel observation period (2018) to prepare a legislative proposal.

What is the role of covered bonds in the composition of the liquidity buffer?

For the LCR, a particular focus of the observation period will be set on the definition of liquid assets. EBA will test different criteria for measuring how liquid securities are under stressed market conditions. This will prepare the ground for a decision before 2015 that will ultimately determine the eligibility criteria for the two tiers of the liquidity buffer.

For the NSFR, the Commission will analyse how such a structural requirement plays out across the diverse EU banking sector, notably as regards its ability to provide long-term funding to support the real economy.

LEVERAGE

Why does the Commission propose to reduce leverage in the banking sector?

Leverage is an inherent part of banking activity; as soon as an entity's assets exceed its capital base it is levered. The Commission does not propose to eliminate leverage, but to reduce excessive leverage. The financial crisis highlighted that credit institutions and investment firms were highly levered, i.e. they took on more and more assets on the basis of an increasingly thin capital base.

What is the Leverage Ratio?

In line with Basel III, the Commission therefore proposes to start the process of introducing a leverage ratio. The leverage ratio is defined as Tier 1 capital divided by a measure of non risk weighted assets.

What purpose does the Leverage Ratio serve?

The purpose of the leverage ratio is to have a simple instrument that offers a safeguard against the risks associated with the risk models underpinning risk weighted assets (e.g. that the model is flawed or that data is measured incorrectly). The ultimate aim is also to reduce leverage in order to bring institutions' assets more in line with their capital.

Will institutions be required to have a Leverage Ratio above a certain value?

Since the Leverage Ratio is a new regulatory tool in the EU, there is a lack of information about the effectiveness and the consequences of implementing it as a binding (Pillar 1) measure. It is therefore important to gather more information before making the leverage ratio a binding requirement. In line with Basel III, the Commission therefore proposes a step by step approach:

Initially implement the Leverage Ratio as a Pillar 2 measure;

Data gathering on the base of thoroughly defined criteria as of 2013;

Public disclosure as of 2015;

Review starting in mid-2016 before a final decision on whether to introduce the leverage ratio as a binding measure as of 2018.

Why does the Commission propose that institutions should disclose their leverage ratio as of 1 January 2015? Does that not effectively make it a binding requirement in view of market pressure?

Requiring the disclosure of the Leverage Ratio is in line with the Commission's push to introduce more transparency in the financial sector in general, and the banking sector in particular. It is also fully in line with Basel III rules. Even in the absence of such a requirement, the market would almost certainly demand institutions to disclose the information on their Leverage Ratio and punish those institutions that would not disclose it by means of raising their cost of capital.

How does the Commission's proposal address the concerns that the introduction of the Leverage Ratio would have significant negative impacts on trade finance and lending to small and medium enterprises, to name just two areas?

The Commission does not currently have sufficient information to be able to estimate the precise impact of the Leverage Ratio. That is why the Leverage Ratio will not be introduced outright as a binding measure, but rather as a Pillar 2 measure (i.e. the judgement on whether or not the leverage ratio of a particular institution is too high and whether that institution should hold more capital as a consequence will be left to the supervisor of that institution). Furthermore, that is why the proposal foresees an extended observation period during which the necessary data will be gathered, and a review to estimate the impact of the Leverage Ratio based on those data that would then inform the decision on the introduction of the Leverage Ratio as a binding measure.

COUNTERPARTY CREDIT RISK

What does the Commission propose to do as regards counterparty credit risk arising from derivatives?

Building on the Commission's proposal for OTC derivatives and markets infrastructures (EMIR) (IP/10/1125) and in line with the Basel III rules, the proposal increases the own funds requirements associated with credit institutions' and investment firms' derivatives that are traded over-the-counter ("OTC derivatives", for further details see MEMO/09/314 and MEMO/10/410) and securities financing transactions (e.g. repurchase agreements).

The proposal also amends the current treatment of institutions' exposure to central counterparties (CCPs) (7) stemming from those transactions, as well as exchange-traded derivatives transactions, in the following way:

Exposures to a CCP will be subject to a non-zero own funds requirement. The size of the requirement will depend on the type of exposure: trade exposures to a CCP (e.g. exposures due to collateral posted to the CCP) will be subject to a substantially smaller own funds requirement than exposures due to contributions to the CCP's default fund. This is because default fund contributions can be used for mutualising losses due to the default of another clearing member.

Compared to exposures from bilaterally cleared transactions, exposures to CCPs will be subject to lower own funds requirements as long as the CCP will meet certain requirements (broadly speaking CPSS-IOSCO recommendations, to be substituted with EMIR requirements once the latter is adopted by Council and EP). If the CCP will not meet those criteria, then trade exposures will be subject to the bilateral treatment and default fund contributions will be subject to a high own funds requirement.

The treatment for exposures to a CCP due to securities transactions (i.e. transactions where the main risk is settlement risk and not counterparty credit risk) will remain the same.

How do the new banking rules proposed by the Commission compare to its earlier proposal on OTC derivatives (EMIR)?

The two proposals complement one another and are fully consistent from the point of view of their objectives and proposed solutions. Both have the same starting point: the financial crisis has exposed the fact that the risks associated with OTC derivatives were not backed by sufficient capital or collateral.

EMIR tackles the abovementioned issue mainly from the point of view of collateral (a means of security to cover for the risk; usually cash). In particular, it requires companies that are active in the OTC derivatives market either to clear those derivatives through a central counterparty (CCP) (this entails providing significant amounts of collateral to the CCP in exchange for the guarantee the latter provides) or, in case this is not possible, to hold collateral to back the risks associated with the derivatives that are not cleared through a CCP. It also tackles the issue of insufficient capital, although to a significantly lesser extent, simply requiring financial institutions to hold appropriate amounts of capital to back those risks.

The new banking rules tackle the abovementioned issue from the point of view of capital. In particular, they determine what the appropriate amount of capital should be in case of banks and investment firms. Importantly, those rules provide for recognition of collateral that a bank or investment firm may already hold to mitigate the risks stemming from OTC derivatives: if those institutions have such collateral then the capital they need to hold can be proportionately lower.

How will this affect corporates and their use of OTC derivatives? Will they not face higher costs when purchasing OTC derivatives from banks?

It is hard to estimate the impact on corporates and other non-financial institutions' use of OTC derivatives. Much will depend on whether banks will be able to pass on their costs to their clients. Regulatory costs are part of the general costs incurred by banks, which they may or may not be able to pass on to customers. This depends on the level of competition in the banking sector. More competition would limit the portion of costs that the banks will be able to pass on.

Irrespective: if the higher cost of using OTC derivatives is the result of the true risk now being included in the price, then that is fully intentional.

Why is the Commission trying to undermine, through the new banking rules, the exemptions granted to non-financial institutions within EMIR?

It does not. The new banking rules are fully consistent with EMIR. EMIR exempts the vast majority of non-financial institutions from having to hold capital and provide collateral when they enter into an OTC derivative contract, as they are exempted from both the clearing obligation and the requirement to hold capital and provide collateral for contracts not cleared by a CCP. However, it was never the Commission's intention to exempt banks from holding capital in those situations. Also exempting banks would mean that the risks the bank faces because of that contract would be backed neither by capital nor by collateral and this would not resolve the problems identified during the crisis.

SUPERVISION

How does the Commission propose to strengthen supervision?

Regulation, no matter how good, cannot overcome poor supervision. The financial crisis brought this point on the agenda. As a result, the EU has already taken steps to strengthen supervision, notably with the creation of the three European Supervisory Authorities and the European System of Financial Supervision (MEMO/10/434).

This proposal strengthens banking supervision further by requiring the annual preparation of a supervisory programme for each supervised institution on the basis of a risk assessment; greater and more systematic use of on-site supervisory examinations; more robust standards and more intrusive and forward-looking supervisory assessments.

CAPITAL BUFFERS

What exactly are you proposing as regards the capital buffers?

On the basis of Basel III, this proposal introduces two capital buffers in addition to the minimum requirements: a capital conservation buffer and a countercyclical capital buffer.

The Capital Conservation Buffer amounts to 2.5% of risk weighted assets, applies at all times and has to be met with capital of the highest quality. The purpose of the buffer is to ensure that an institution is able to absorb losses in stressed periods that may span a number of years. Institutions would be expected to build up such capital in good economic times. If banks breach the buffer, they will face limits on paying out bonuses and dividends.

The purpose of the countercyclical capital buffer is to achieve the broader macro-prudential goal of protecting the banking sector and the real economy from the system-wide risks stemming from the boom-bust evolution in aggregate credit growth and more generally from any other structural variables and from the exposure of the banking sector to any other risk factors related to risks to financial stability. . It will be applied by adjusting the size of the buffer range established by the conservation buffer by up to additional 2.5%. The countercyclical capital buffer is set by national authorities for loans provided to natural and legal persons within their Member State. It can be set between 0% and 2.5% of risk weighted assets and has to be met by capital of the highest quality. If justified, authorities can even set a buffer beyond 2.5%. This buffer will be required during periods of excessive credit growth and released in a downturn. The ESRB could issue recommendations for the buffer settings by national authorities and its monitoring, including instances where the buffer exceeds 2.5%. So long as the Countercyclical Capital Buffer is set below 2.5%, Member States have to mutually recognise and apply the capital charge to institutions in their Member State. For parts of the buffer exceeding 2.5%, authorities can choose if they accept the judgement of their peers and apply the higher rate or leave it at 2.5% for institutions authorised in their Member State.

Credit institutions and investment firms whose capital falls below the buffers will be subject to restrictions on the distribution of profits, payments on Additional Tier 1 instruments and the award of variable remuneration and discretionary pension benefits. In addition, these institutions will have to submit capital conservation plans to the supervisory authorities to ensure a swift replenishment of the buffers.

Why are these buffers necessary? Would it not have been sufficient to increase the minimum level of required own funds?

The buffers serve a somewhat different purpose.

The capital conservation buffer provides an additional cushion of capital to absorb losses to prevent the situation in which taxpayers' money would have to be injected for recovery and resolution of institutions from reoccurring. This buffer sits on top of the minimum requirements. Accordingly, if banks breach the buffer (capital ratio below 7% RWA), they face restrictions on their dividend and bonus payments. This is important. During the crisis, many banks continued to pay out dividends even as they were experiencing problems. This eroded their capital base. The buffer's capital retention measures prevent this.

As regards the counter-cyclical buffer, it is meant essentially to stabilise the supply of credit to the economy, thereby making sure that bank rules do not amplify economic cycles. It therefore forms part of a new generation of so-called 'macroprudential' tools, i.e. tools not so much focused on the individual health of an institution but focusing on the effects of regulation on the financial system as a whole.

What about systemically important banks?

The treatment of systemically important financial institutions (SIFIs), of which systemically important banks form part, is currently subject to discussions at the Financial Stability Board and the Basel Committee on Banking Supervision (BCBS). The FSB and BCBS issued a public consultation on 20 July. (8) A detailed framework will be submitted to the meeting of G-20 leaders at Cannes on 3-4 November 2011 for their decision. It is accordingly premature to include any requirements related to systemically important banks in this proposal.

CORPORATE GOVERNANCE

How will the proposal improve corporate governance?

The proposal will introduce clear principles and standards applicable to corporate governance arrangements and mechanisms within institutions. These principles and standards will concern the composition of boards, their functioning and their role in risk oversight and strategy in order to improve the effectiveness of risk oversight by Boards. The status and the independence of the risk management function will also be enhanced. Supervisors will play an explicit role in monitoring risk governance arrangements of institutions.

The measures envisaged should help avoid excessive risk-taking by individual credit institutions and ultimately the accumulation of excessive risk in the financial system. The principle of proportionality, taking into account the size and complexity of the activities of the credit institution as well as different corporate governance models, will apply to all measures.

Corporate governance – will you impose diversity ?

Diversity in board composition should contribute to effective risk oversight by boards, providing for a broader range of views and opinion and therefore avoiding the phenomenon of group think.

The measures proposed will require credit institutions to take diversity into account as one of the selection criteria of members of the board. To ensure consistency with the horizontal Commission initiative with regard to gender balance on companies' boards, the proposal will not at this stage introduce any specific quantitative objective with regard to the presence of women on boards of credit institutions or investment firms.

Why reforming only CRD IV (banks and investment firms) and not other sectors (insurance, investment funds)? This may lead to inconsistencies between different sectors and it is difficult to justify why in banks there should be a limitation of the number of mandates, separation between CEO/Chair, board diversity, and not in insurance companies or investment funds.

The corporate governance failings which contributed to financial crisis occurred mostly in banks. The Commission does not have convincing evidence of the same problems with regard to governance systems in insurance companies or investment funds. Also, existing rules in the banking sector are of a very general nature as compared to insurance or investment fund legislation where rules on internal organisation and risk management are much more detailed and precise. That is why we start with reforming corporate governance in credit institutions and investment firms. However, for the sake of consistency and in order to avoid regulatory arbitrage between sectors, it will be necessary to review the existing legislation in other sectors (Solvency II, UCITS Directive) to align it, when necessary, to the outcome of the final text of CRD IV package. Nevertheless, the specificities of each sector should be taken into account, and the rules should not necessarily be identical for banks, insurance companies and investment funds.

SANCTIONS

What exactly is the Commission proposing regarding sanctions?

The proposal will require Member States to provide that appropriate administrative sanctions and measures can be applied to violations of EU banking legislation. For this purpose, the Directive will require them to comply with common minimum standards on:

types and addressees of sanctions,

the level of fines,

the criteria to be taken into account by competent authorities when applying sanctions,

the publication of sanctions,

the mechanism to encourage reporting of potential violations.

These provisions are without prejudice to the provisions of national criminal law.

Why is the Commission proposing provisions on sanctions in the revision of the CRD?

The "CRD IV" package fundamentally overhauls the substantive prudential rules applicable to institutions. But these rules will only achieve their objective if they are effectively and consistently enforced throughout the EU. This requires that competent authorities have at their disposal not only supervisory powers allowing them to effectively oversee credit institutions but also sufficiently strict and convergent sanctioning powers to respond adequately to the violations (which may nevertheless occur), and prevent future violations.

However, the banking sector is one of the areas where national sanctioning regimes are divergent and not always appropriate to ensure deterrence.

For example, in the banking sector the maximum amount of fines provided for in case of a violation is unlimited or variable in five Member States, more than 1 million euro in nine Member States, and less than 150 000 euro in seven Member States. Those maximum levels, in the latter group in particular, appear to be rather small, especially in view of the large size of the banking groups operating in several of these States. For more examples see MEMO/10/660

Therefore, the Commission proposes the introduction of rules to reinforce and approximate national sanctioning regimes.

Banking supervision is based on supervisory measures to prevent violations and restore banks' viability – why would sanctions be necessary?

When a bank is in distress, the first priority is in fact to save and not to sanction it.

In fact, the Commission does not propose harmonised sanctions for violations of minimum capital requirements.

But sanctions are key to ensure other rules are respected – for example if banks don't report to supervisors as required, and thereby make supervision ineffective, or if banks act without authorisation.

What is the Commission planning to do to ensure that breaches are actually prosecuted and that appropriate sanctions are actually handed down?

Our initiative makes sure that all supervisors have the possibility, that is to say are empowered, to impose effective sanctions. National supervisors remain mainly responsible for the actual application of sanctions.

In order to ensure that breaches are actually prosecuted and ensure convergence for sanctions handed down, we require supervisors to put in place whistle blowing programmes to improve detection of violations, and propose convergence on the factors to be taken into account when imposing sanctions in each individual case.

Prosecution is highly case specific and in the realm of national authorities (with the exception of Credit Rating Agencies), so the reach of EU legislative action is limited. Therefore, peer reviews conducted by the ESAs (Art 30(2)(d) of the ESA Regulations explicitly refers to sanctions) are an important tool to ensure further convergence, and once the legislative framework in all Member States on what supervisors can do will have converged following our initiative, we place big hopes in them.

What has happened to the idea of criminal sanctions?

Criminal sanctions can have an important deterrent effect in particular on individuals, and can therefore be appropriate in certain instances. Under Art 83(2) TFEU, the EU can take action on criminal sanctions but only under limited circumstances. We will further assess whether EU action on criminal sanctions is necessary for the financial services area as a whole and will decide about appropriate further action on that basis.

List of violations for which sanctioning powers should be available:

unauthorised banking services;

requirements to notify authorities in case of acquisition of qualifying holdings;

governance requirements;

reporting requirements on capital, liquidity, leverage, large exposure;

limits on large exposures;

retention requirements on securitisation;